As Gen X—an often-overlooked generation—takes on greater leadership and gains more affluence, now’s the time for a step-by-step financial strategy for all future generations.

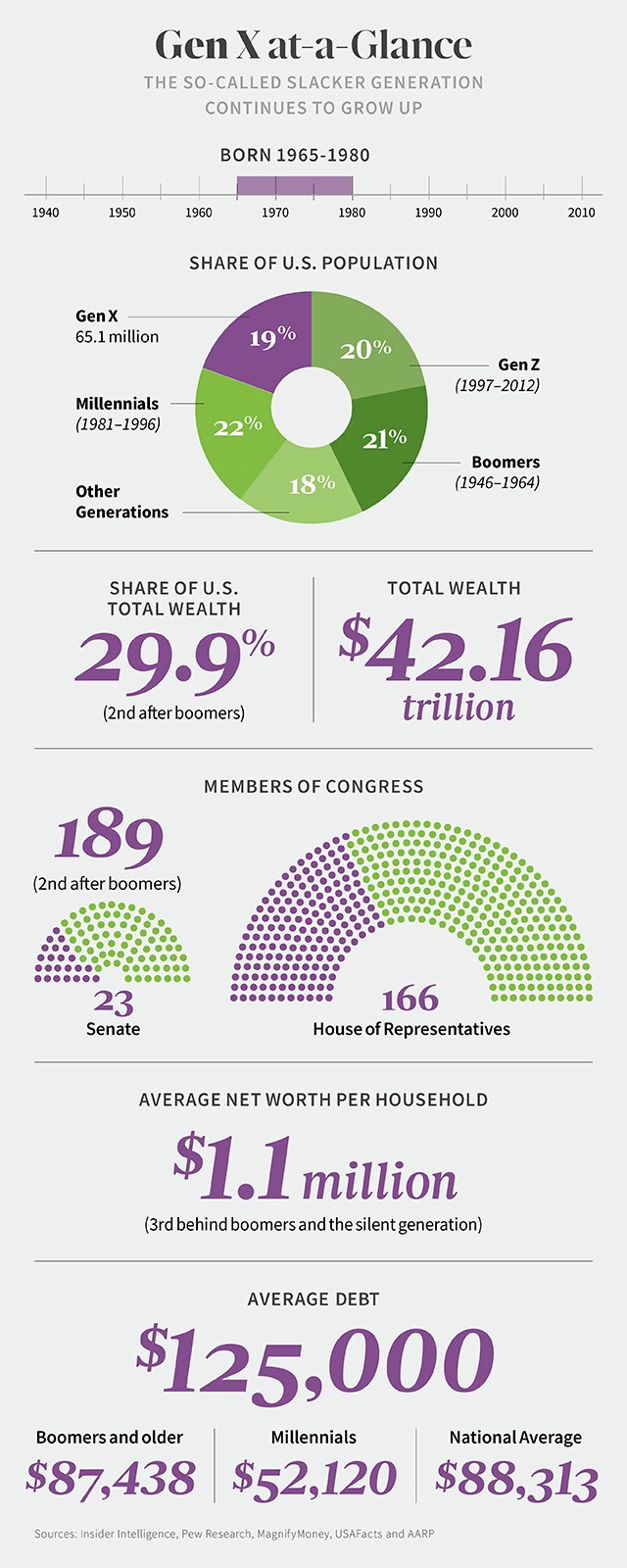

Wedged between the larger and louder baby boomers and the much-ballyhooed millennials, members of Generation X (born between 1965 and 1980) have sometimes struggled to get noticed at all. While boomers defined postwar America in all its optimism, and millennials (now the biggest generation by numbers) are redefining life as the first fully digital generation, Gen Xers were once famously described as “America’s neglected ‘middle child.’ ”

Yet that image is changing as Gen Xers, ranging in age from their early 40s to their late 50s, assume a greater share of the nation’s leadership in everything from politics to wealth. They occupy about 35% of seats in the Senate and House of Representatives, for example. As they come into inheritances and reap the rewards of their entrepreneurial and professional success, Gen Xers now control more than $42 trillion in personal wealth. As a result, members of this generation are taking a larger role in managing their own—and the nation’s—wealth. Some inherent qualities and experiences make Gen Xers well-suited for the role.

Though still in mid-career, they’ve endured numerous global financial upheavals, including the Great Recession, and assumed outsized responsibilities as a “sandwich” generation, supporting the needs of their parents and kids while navigating their own lives. “Still, the challenges of wealth stewardship require a concerted approach to organizing and managing short-term and long-term needs,” says Tony Allen, Senior Vice President and Private Wealth Leader at Regions Bank in Birmingham, Alabama.

If you count yourself among Gen X or a younger generation, the following ideas could help you meet your own goals and instill strong financial values for generations to come.

Think Digitally

Though they’re the last generation to have experienced adulthood in a pre-internet world, Gen Xers came of age amid the digital transformation and are apt to be more comfortable than boomers at embracing its conveniences. That comfort gives Gen Xers the freedom to manage wealth from anywhere. If you haven’t done so already, your Wealth Advisor can help you set up a full suite of digital tools, including secure online and mobile banking, money transfer and bill paying options, text banking, automatic alerts and notifications regarding account balances.

Beyond the freedom and convenience digital tools offer, having all of your information (from one or multiple financial institutions) in a single, secure portal can help you organize and manage your finances, track your savings and spending, establish and maintain a budget, and monitor cash flow.

Assemble the Right Team of People

“As comfortable as digital transactions become, they’re no substitute for the value of professional guidance,” says Allen. A digital-only approach may not address the nuances of your personal situation and could leave you turning to friends and family for ideas and strategies. Th is may be especially true if you come into sudden wealth, through either an inheritance or professional success. “However well-intentioned a friend’s advice may be, an experienced Wealth Advisor can help you consider opportunities and risks in a balanced way and build an investment portfolio designed to grow and help you pursue your goals, while managing risks,” says Allen.

Additionally, your Wealth Advisor can act as the captain of a team that includes estate and trust specialists, attorneys and tax professionals who, together, will view your money, your family and your goals from every angle, and suggest the best ways to prepare for the future.

Clarify Your Goals

Managing your wealth over your life is easier when you have clear destinations in mind. “Even if you’re certain you already know what you want to achieve, taking the time to write down your goals and how much time you have to achieve them can help sharpen and clarify your objectives,” says Allen. Then, you can identify which priorities are most important and gauge the resources needed to get there.

Retirement is a good place to start. “Though your working days are far from over, the sooner you start planning, the better,” says Christopher E. Ritchie, the Private Wealth Market Leader for Arkansas. At what age do you hope to retire? Where will you live, and what lifestyle do you envision? Will you travel extensively, continue working part time or volunteer?

While these goals will continue to evolve, considering them now can help you determine what to set aside in taxable and tax-advantaged accounts, and how to invest in order to provide the income you’ll need after you stop working.

Next, list important needs that may arise sooner. Perhaps you envision a mid-career switch to a pursuit that pays less but fulfills a dream. Or you hope to purchase a vacation property while ensuring you’ll be able to support education for your family. Even if your children are still very young (or you’re planning a family but haven’t started), it’s never too early to start a tax-advantaged 529 savings plan to meet the rising costs of education. Money you put into a 529 can grow and be used for tuition or other approved education-related expenses for children, grandchildren or other beneficiaries.

Build a Diversified Portfolio

However you’ve gained wealth, whether through the sale of a business, an inheritance or other means, protecting and growing it requires a strategic plan. “Spontaneous, fad-based decisions could put your money at risk, especially if you’re inexperienced at managing wealth,” says Allen. At the other end of the spectrum, inaction can be just as problematic. For example, keeping all or most of your money in shares of a single company or property poses outsized risks, should those assets decline in value.

Th e best approach is to diversify your wealth in a portfolio that contains a broad mix of assets of different types, whether stocks, bonds or alternative investments. Your Wealth Advisor can help you build a portfolio that creates opportunities for long-term growth, generates income and mitigates risk.

A portfolio should be designed with your personal risk tolerance in mind. “Regardless of what your portfolio contains, if the risks have you tied in knots with worry, you may want to adjust to a mix that feels more comfortable,” says Ritchie. As your comfort level increases, you’ll be more likely to resist selling when you shouldn’t. Indeed, making a commitment to stick with your plan is just as important as starting one. “When investors react to market swings with emotion, they tend to make poor investment moves, such as buying high and selling low,” he says.

Set a Course for Tax Efficiency

Any financial decision you make will have tax implications. Considering these carefully before acting can help ensure you have more money to pursue your own adventures and to support the people and causes you care about. One straightforward example is making sure you contribute the maximum allowable amounts to 401(k)s, IRAs and other tax-advantaged retirement savings accounts. Also, think carefully about which investments should be held inside or outside those accounts. Investments you hope will grow over time may especially benefit from tax protection. Other investments, such as municipal bonds, which already come with tax advantages, may be best held in taxable accounts.

If much of your wealth is concentrated in a single asset, such as shares of a company or a large real estate holding, selling off pieces of those assets and investing elsewhere could help you diversify and reduce risk, as mentioned above. “But be careful about selling too quickly,” Ritchie says. “If the asset you own has climbed in value, a sale may trigger significant capital gains taxes.” Your team may be able to suggest strategies for selling over an extended time, in a way that diversifies your holdings while minimizing capital gains.

Anticipate Health-Care Costs

With medical costs rising each year, health care is another area where long-term tax efficiency can make a difference, Ritchie notes. Consider creating a tax-advantaged health savings account, or HSA, to help you meet estimated out-of-pocket health-care expenses in retirement—though you can only contribute if your current health insurance is a qualified high-deductible health plan. Contributions, investment growth and withdrawals for qualified medical expenses are all potentially tax-free.

Any funds in your HSA can roll over year to year and be invested to grow over decades, making this kind of account a particularly powerful way to save for future medical expenses. And while it may be hard right now to envision a time when you’ll need it, studies show that 70% of Americans over age 65 will require long-term care.

One way to cover current medical expenses with tax-advantaged dollars is to open a flexible spending account, or FSA. An FSA enables you to put income you won’t be taxed on into an account, sponsored by your employer, that you can use to meet health-care expenses not covered by your medical insurance. The downside: FSAs generally require you to spend most of your contributions by the end of the year or risk forfeiture. Your team can help you consider the options.

Consider Your Legacy

Your 40s and 50s are good times to consider what you’d like your wealth to achieve beyond your lifetime, whether supporting your children, grandchildren and future generations, or your long-term philanthropic goals—or all of them. To start, be sure to create a will if you haven’t done so yet. Or, if you have a will but haven’t reviewed it recently, make sure it reflects your current circumstances and wishes. “Updating this and other legal documents will ensure the right people and organizations will benefit from your wealth and that your preferences for how it’s distributed will be honored,” Ritchie says.

You might speak with your Wealth Advisor about ways that trusts could help protect your wealth for the next generation and beyond. Irrevocable trusts can help ensure that distributions will go to beneficiaries you designate, and can protect assets from outside creditors, ex-spouses (in case your beneficiaries are divorced) and others. In short, “a trustee oversees the trust and applies a standard for distributing the assets according to your directions,” Allen notes.

At the same time, your team can help you identify your charitable goals and create a tax-efficient plan that maximizes the impact you can have. That may include creating charitable trusts and/or a donor-advised fund, or DAF. With a DAF, for example, you can make a large, upfront contribution to offset a spike in income in a given year, and then distribute the proceeds at a pace that you see fit.

Pass Down Your Financial Wisdom

As you prepare yourself financially for the years ahead, use what you’ve learned to help the next generation get a leg up on financial fitness. According to one frequently cited study, adults save only about half of what they inherit. Instilling sound budgeting, spending, saving and investing habits in your kids will likely pay off in the long run.

Start by having open conversations about money, your views on wealth and your values. “While portfolio strategies and tax efficiency are important,” says Ritchie, “preserving wealth across generations also involves instilling in the next generation the values that went into building that wealth.”

Talk to Your Regions Wealth Advisor About:

- How trusts could help protect and preserve your wealth over generations.

- What your financial and personal goals are. How does your retirement look different from your working life?

Interested in talking with an advisor but don’t have one?

Find a contact in your area.