Buried under credit card debt? Here's how to get out from under it.

Shouldering the burden of one or more high-interest monthly debt payments isn’t easy. Even the mere thought of dealing with debt can feel overwhelming, keeping us up at night.

Yet it doesn’t have to be that way. By learning best practices—using credit cards wisely, adjusting your budget, tweaking your spending and developing a repayment strategy—getting out from under debt is possible.

“People who use credit cards wisely understand that purchases are loans,” says Kimberly Cobb, Financial Wellness Relationship Manager at Regions Bank. “That means either they’re able to pay off those loans within their regular budget, or they have a plan to pay off the balance over time for larger purchases.”

Here are smart strategies for dealing with existing credit card debt and for strengthening your credit over the long term.

Dealing With Debt

Understanding your spending habits is the first step toward changing them. The good news is that financial awareness goes a long way—and you can start paying attention right now. Start with these strategies:

Review your statements. As soon as credit card statements come into your email inbox or your mailbox, review them. That’s the best way to learn when and where you use your credit card the most, and spot any unauthorized charges.

Set up alerts. “Email or text alerts that coincide with your statement date, bill due date or both can trigger you to pay those bills on time,” says Cobb. Consider setting up autopay so you’ll never miss a payment, and you can avoid late payment fees.

Review spending categories. Many credit card platforms break down spending into categories like entertainment and groceries. Simply by regularly checking your statements, you’ll see the areas where you are most prone to overspending. Cutting back might be easier than you think, and no, you don’t necessarily need to sacrifice that coffee fix or self-care routine. “A lot of times, people will find expenses they forgot, such as subscriptions or memberships they’re no longer using. Digging in can help you reroute some less important discretionary spending toward paying off debt.”

Create a budget. A budget can help you understand your spending patterns and figure out where to cut back. “Make a list of needs, such as housing, groceries and transportation. Then identify the expenses that are ‘wants,’ or discretionary spending, and start there to see what can be eliminated or reduced,” says Cobb. “Wants might include dining out, subscriptions, cable, manicures or entertainment.”

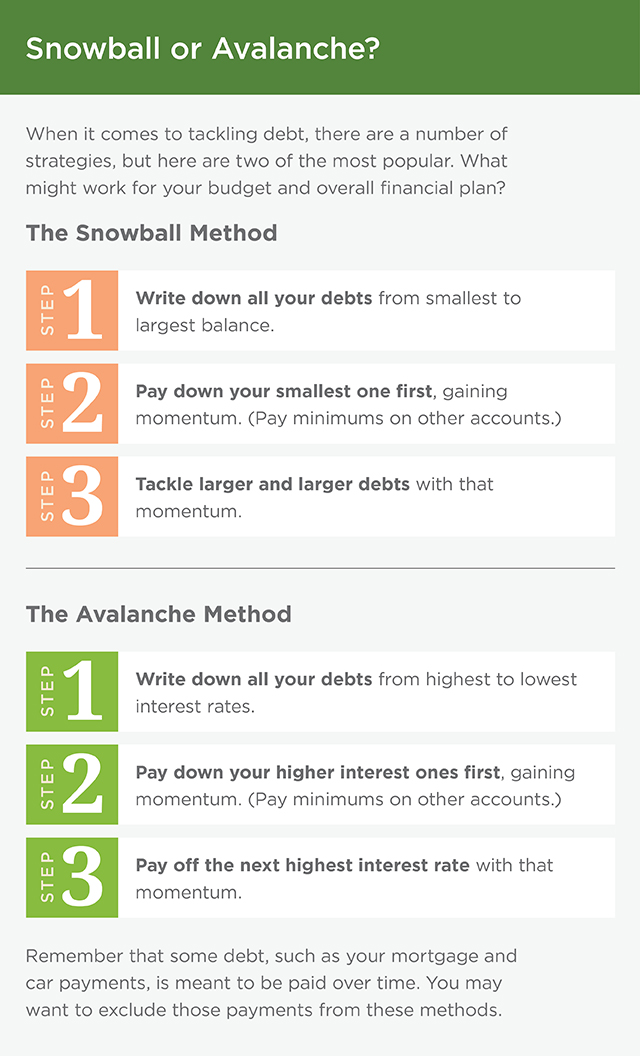

Develop a repayment strategy. Once you’ve budgeted extra money for repayment, explore different debt repayment approaches, find one that works for you and, most importantly, stick with it. Here are two of the most popular.

Set a repayment goal. Whether it’s making on-time payments for a full year or knocking out the biggest debt in months, goals foster good habits and accountability. Consider sharing your goal with a family member or friend who can provide support, or chart progress on social media. Whatever works for you is the right approach.

Maintaining Good Credit

As you chip away at those balances, the next step is making sure you don’t undo that amazing progress. These tips can help you keep your debt under control—and boost your credit score in the process.

Use credit responsibly. “Credit card issuers want to see that you manage credit responsibly, so don’t be afraid to use your credit card,” explains Cobb, noting that it’s important not to max out credit cards and to keep your utilization rate lower than 30%.

Check your credit report. Cobb recommends obtaining a free annual credit report from each of the three major credit bureaus to check for discrepancies or errors that could be dragging down your credit score. If there are mistakes, it’s important that you take the time to dispute and correct them.

Monitor your credit score. Your credit score impacts your entire financial life. “The higher your credit score, the less risk you present to lenders, and typically, the better your interest rates will be when you’re shopping for a larger purchase,” Cobb says.

Take advantage of rewards. Whether you’re using your credit card for gas, groceries or other repeated purchases, reap as many benefits as you can, says Cobb. Let’s say you use your credit card only for groceries and gas. If that’s the case, make sure you have a card that offers points or cash back for those spending categories, and, says Cobb, “make sure you have a plan for paying it off. If not, your rewards might quickly be offset by more high-interest debt.”

Pay attention to interest rates. “People often sign up for credit cards to take advantage of sign-up bonuses that offer a 0% interest introductory rate,” explains Cobb. But because credit card rates are typically not fixed, that rate might change significantly after your intro period is up.

Three Things to Do

- Take an online financial education course on building and maintaining credit.

- Explore the rewards offered by credit cards, which can be a boost for your budget if you use credit responsibly.

- Learn about credit card fraud—and how to avoid it.