Stocks Commentary

Stocks: ‘Momentum,’ Fundamentals Supportive, But On The Lookout For A Mid-Year Lull

June 2026

U.S. equity indices followed up April’s rally by tacking on sizable gains in May, with the S&P 500 rising 5.2% during the month behind strength out of AI-related names - primarily semiconductor stocks. Impressively, the broader index was higher by 11.2% year-to-date on a total return basis through May after a trough-to-peak move of 19.7% off the late March low. The fundamental underpinning of U.S. stocks, i.e. the earnings outlook, continued to brighten throughout May with earnings season providing market participants with ample reasons to remain allocated to U.S. stocks despite the proverbial ‘wall of worry’ equity markets continue to climb.

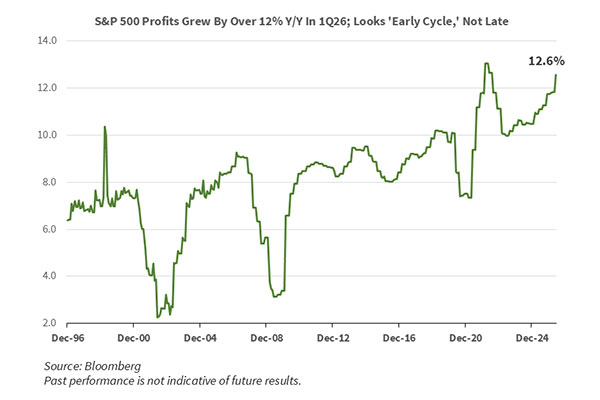

At the end of March, as the U.S./Iran conflict drug on and the potential long-term impacts it could have on the energy market and crude oil prices dominated discussions, while the consensus estimate for full year 2026 earnings per share (EPS) out of the S&P 500 index sat at $323. But with both trailing results and forward guidance surprising to the upside as quarterly reporting season ramped up in mid-April, the ’26 EPS estimate moved to $333 at the end of April and continued to rise in May, ending last month at $339. Upward revisions of this magnitude in such a short period of time have historically occurred at the start of economic cycles, not in the middle or toward the end of an economic expansion. But this time around sell-side prognosticators are coming around to the idea that this economic cycle could very well be different due to the mania and frenzy surrounding the buildout of AI-related infrastructure.

With earnings estimates moving markedly higher in recent months, the S&P 500 closed out the month of May trading at 22.5 times projected 2026 earnings, which is lofty by historical standards. However, once we pass the midpoint of this year market participants will begin to shift their focus to the 2027 outlook for profits and this pivot could be a source of further upside for U.S. large cap stocks as the current 2027 EPS estimate of $390 leaves the S&P 500 trading at 19.5 times next year’s estimate. While not part of our base-case scenario, assuming the move lower in crude oil prices in late May is sustained and keeps a lid on interest rates, the S&P 500’s current price-to-earnings multiple could even expand modestly from here, in our view.

U.S. small and mid-cap (SMid) stocks have also seen earnings estimates move higher in the past couple of months, albeit not to the same degree as the S&P 500, and lower energy costs and falling interest rates will provide tailwinds for smaller companies to varying degrees. However, smaller capitalization stocks could see tougher sledding as the initial public offering (IPO) window opens this month with SpaceX set to go public, and given SMid is a higher beta cohort of stocks that have done well of late, some high flyers in these indices could see profit taking as investors look to fund allocations to newly public investments. Also worth watching, should U.S. economic growth hit a soft patch as is common in the lead-up to midterm elections, these stocks could experience relative weakness as investors turn to higher quality, dividend paying names in the S&P 500 as they ride out heightened economic and/or political uncertainty.

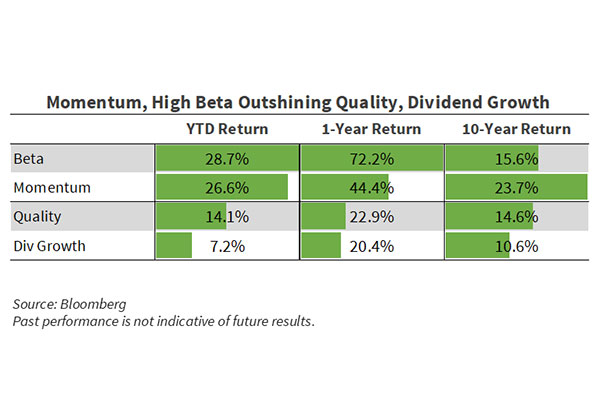

One blemish that continues to be fodder for market bears is the narrow breadth off the late March lows, as outside of the information technology sector returns at the sector-level have largely been unspectacular. The factor leadership profile also gives us pause as ‘momentum,’ and high beta names have led while ‘quality’ factors have lagged materially. While this is a sign of healthy investor risk appetite, it’s also potentially worrisome as ‘momentum’ can be fickle. Just as positive momentum can propel prices higher, a loss of momentum can lead to a sizable and unsettling drawdown in a short period of time as renters of these stocks look to sell early once the trend rolls over and reallocate capital into the next best thing. Another variable worth watching in the next few months is a potential flurry of IPOs to see how orderly markets digest these sizable, high-profile new issues. On balance, we see the earnings outlook and positive momentum behind AI-beneficiaries offsetting narrow breadth and liquidity concerns surrounding the wave of IPOs, but after such a sizable move off the March lows, a midyear lull and a period of consolidation would likely be healthy and set U.S. equities up on firmer footing for a year-end rally following the midterms in November.

As of June 10, 2026

Related Insights

-

Article

6 min read

Article

6 min read

-

Article

11 min read

-

Article

12 min read